Buffett is referring to Howard Marks, the chairman of Oaktree Capital, who writes regular investing commentaries on the Oaktree website (click here) and is the author of The Most Important Thing: Uncommon Sense for the Thoughtful Investor (2011). I've been a regular reader of Marks' commentaries for a few years, but somehow - regrettably - only picked up his excellent book this past week. If you're passionate about investing, it's a must-read.

This week I'd like to build upon a piece of advice from his book on the importance of building and keeping a watchlist of ideas:

Having a watchlist of potential investments next to your workstation allows you to more effectively seize upon opportunities presented by the sometimes-mercurial Mr. Market. Armed with a watchlist, the patient investor will be at an advantage as he or she can simply wait for good investments to arise rather than going out looking for them. But there's a difference between a good watchlist and one that you've scratched on the back of an old grocery shopping list (something I've been guilty of now and again) or keep locked up in your mind where it's sure to be forgotten or warped to fit your sentiment du jour. Fortunately, Marks provides us with the key criteria of a good watchlist -- namely a fair value estimate, a measure for margin-of-safety, and a risk assessment of each investment.

Trouble is, determining the intrinsic value for a stock can not only be a complex process, but it can also be very time-consuming. For individual investors that struggle to find time to research stocks between jobs, family time, and other pursuits, intrinsic value estimation can seem a futile endeavor. I reckon that's why many investors rely on rules-of-thumb (i.e. "buy only low P/E stocks") or tips heard from friends or in financial media when making investment decisions. It's a natural response to look for quick fixes when we're short on time, but if we hope to achieve superior investment results, it's essential that we find a way to consistently purchase securities below their fair value and -- perhaps more importantly -- to avoid investing in overvalued securities.

Listen to the market

While investing contains many uncertainties, we do have one objective piece of information to rely on -- the stock price. The stock price gives us an incredible amount of information about the market's active assumptions for a given security.

If we make the fair assumption that the intrinsic value of a security is the discounted value of its future dividend payments (Gordon Growth Model), know the latest annual dividend payment, and can make a reasonable discount rate estimate, we can determine the market's current growth assumptions for the dividend.

Where:

Current market price = (Dividend per share * (1+Growth))

------------------------------------------------

Discount Rate - Growth

***You can also use next year's estimated dividend as the numerator

In other words, if a stock's market price is $100 per share, the latest annual dividend was $2 per share, and the appropriate discount rate is 10.5%, we can algebraically determine that the implied growth rate at that price by calculating:

$100 = $2 * (1+Growth)

----------------------

10.5% - Growth

In this case, the market's implied long-term dividend growth rate at $100 is 8.33%.

That's powerful insight to have as an investor. By estimating the market's implied growth rate, we can then determine whether or not the market's growth assumption is reasonable (therefore making the stock nearly-fairly valued), too high (overvalued), or too low (undervalued).

This leads us to yet another problem, though -- how do we know if the implied growth rate is reasonable, too high, or too low? That is the million-dollar question, of course. If it was an easy answer and everyone knew it, the stock would be perfectly priced because everyone would have the same assumption. Frankly, most of the time the market's estimate is fairly good, which leaves few opportunities to take advantage of mispricings. However, it's still worth determining your own growth estimate because every so often the market graces us with good buying and selling opportunities -- Mr. Market can quickly become a distressed seller offering fire-sale prices or can be euphoric and ready to offer you top-dollar for your stock. In those situations, the emotional Mr. Market pays little attention to reasonable growth estimates and is just looking to make a deal. And that's when the prudent investor should be ready to pounce.

One way to estimate a long-term growth rate is with the "sustainable growth rate" formula, which is simply:

SGR = Return on Equity * Retention Ratio

Where: Retention Ratio = (1-dividend payout ratio), or (1-(1/dividend cover))

What this formula tells us is that if a company is generating a return on equity of 15% and is paying out 50% of its earnings in dividends, the 50% of its earnings that it's retaining can be reinvested in the business at 15%. The sustainable growth rate is therefore 15%*50% = 7.5%. This is the highest growth rate the company can generate without increasing leverage (increased leverage would, all else equal, increase ROE).

If we plug this 7.5% growth assumption into the previous example where the $100 market price was implying an 8.33% growth rate, it's possible that the stock is overvalued as the market could be overestimating the company's future growth. At the very least, it opens up some valuable questions to be answered with further research such as "Why might the market be pricing in higher growth -- is it a function of a higher potential return on equity, a higher retention ratio, or a combination of both?"

Getting started

Circling back to the point of these formula explanations, a simple DDM and SGR calculation can be effectively used in a watchlist of ideas by helping you determine a stock's intrinsic value. To get you started, I've created an example watchlist on Google Docs, which you can download (free, of course) by clicking here.

The "Watchlist" tab contains the key elements that Marks advocates in a good watchlist -- a fair value estimate, margin of safety, and risk factors. You'll need to enter the data points manually and update them often. (Click image to enlarge)

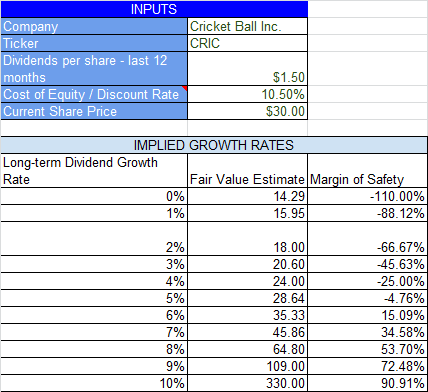

The "DDM Valuation" tab contains a DDM tool that can help you determine the implied dividend growth rate of a stock at various market prices. You only need to enter a few data points -- the current stock price, the trailing twelve month dividend payout, and an estimated cost of equity (for most large, stable companies a 10.5% cost of equity is a fair baseline assumption). In the default example, the $30 per share market price of Cricket Ball Inc. implies the market is pricing-in a long-term dividend growth rate near 5% assuming a 10.5% discount rate and given its $1.50 per share dividend last year. If Cricket Ball Inc. could grow its dividend at 6%, it might be worth $35 and at 7%, $46, and so on.

There's also a simple sustainable growth rate calculator on the "DDM Valuation" tab, which could help you determine a reasonable growth rate assumption for the stock you're researching. You'll need to input the 5 year average return on equity and the retention ratio. In the default example, Cricket Ball Inc.'s five year average ROE was 12.5% and it retained 55% of its earnings last year, which results in a sustainable growth rate of 6.88%. If Cricket Ball Inc. can indeed sustain a 6.88% growth rate, its fair value should be approximately $44 -- again assuming a 10.5% cost of equity -- and that would provide a 32% margin of safety at current prices near $30, making it a reasonable buying opportunity.

Proceed with caution

By no means is the DDM a perfect valuation model (it works best with stable companies with a history of dividend payouts) and the "garbage in, garbage out" rule applies as with any calculation, so be sure to double-check your data points for accuracy. I encourage you to combine the DDM results with other valuation methods to determine a range of possible values. The DDM can, however, provide some valuable insight into the market's current growth estimates and is a fairly simple way to get started with determining a stock's intrinsic value. At the very least, it's better than making buy/sell decisions with no grasp of intrinsic value, which would ultimately lead to poor investment decisions and subpar results.

I hope this discussion and sample watchlist will help you make better investment decisions. And do yourself a favor and buy Howard Marks' book! Let me know what you think of it.

Stay patient,

Todd

@toddwenning on Twitter